Walking the show floor at Money 2020, one sees lots of payment providers. Its no shock then that today, I saw a lot of talks on how this works. This is in keeping with the theme of the show: the future of money. The previous two days, I did hear a fair amount of talk about moving away from paper money, what to do about fiat currency vs. other currency, and difficulty in managing payments. Today, we heard about what is possible with payments.

The facts keep stacking up around us about people preferring to pay electronically instead of with plastic or currency. Those electronic payments are happening in apps:

The first three are as phone OS capabilities, the last two are via apps on the phones. Electronic payments make a number of things better for consumers, retailers, and credit institutions (banks, credit card companies, etc.). For consumers, they get convenience. For retailers, they find less friction at checkout. For credit institutions, they get reduced fraud. So far, so good, right? Well, what I learned after this was a lot more interesting: if you are just reducing payment friction, you are leaving a lot of opportunity on the table. Opportunity for:

- Learning about the customer. You are collecting their buying habits. Imagine what you could do if you did more to help, what else could you learn?

- Getting retailers to use your payment system. You know a lot about your customers and what they like to buy. You can now refer them to other retailers, services, and so on. Use that to convince retailers that if they use your system, you will drive more interested customers their way.

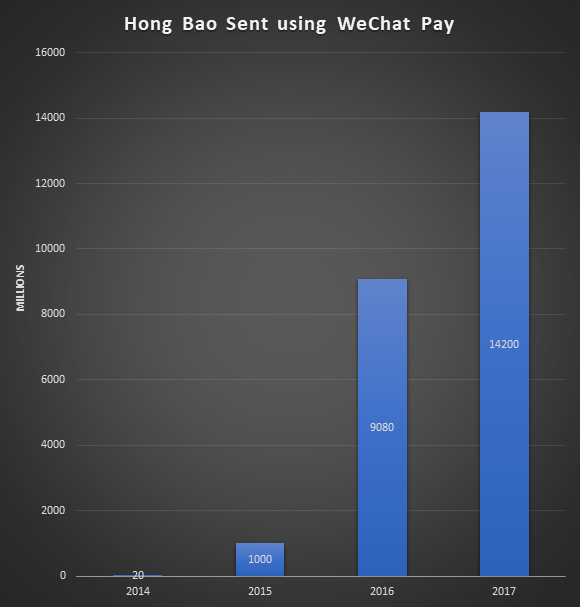

- Delight your customers in novel ways. WeChat has delighted their Chinese users by making it easier to send Hong Bao (a monetary gift in a red envelope) to others. Their users love this feature. Here’s what the growth has looked like year over year (numbers are from a presentation by Ashley Guo of WeChat):

You can also look at Ant Financial/Alipay. Despite their name, they are not a payment company; they are a marketing company. You use them to schedule doctor appointments, figure out how to travel on public transportation or taxi, manage vacations, discover information about products, and so on. And yes, when the service is performed or goods are purchased, they also make sure that the vendor is compensated by you. But, they make it all seamless. The product has been successful in China, turning their tier 1 and tier 2 cities into cashless areas. The services are so popular with their Chinese user base that the apps are used around the world at high end retailers down to businesses like Burger King.

Both WeChat and Alipay emphasized that they use the data to better market to users. The users like the targeting in their lives. When traveling, they discover attractions and restaurants that appeal to them because the app knows them so well. The businesses are happy to participate because they acquire customers who may not have found them otherwise.

What I saw today was a lot of companies thinking about how to make transactions easier by working with banks and credit card companies to remove plastic from your life. This is great. I look forward to the day when my wallet no longer bulges because of all the cards I need to carry.

I also saw something wonderful and scary: a world where things will generally improve for me if I let artificial intelligence and machine learning see all the things I do. By knowing what I eat, where I go, and so on maybe the algorithms can warn me to start doing some things (walk more) and stop doing other things (keep it to two coffees a day). Scary, because I worry what would happen if all that data was combined in some nefarious way. For example, if the algorithm senses that I get out of depression by spending money, maybe the algorithm seizes on this by getting my spending up using knowledge sales people only wish they knew. Or, me being denied a job because the data leaks that I buy [something the employer wants to look out for: alcohol, cigarettes, etc.].

In all, a very interesting day around payments.

You must be logged in to post a comment.